example.com

Verify you are human by completing the action below.

example.com needs to review the security of your connection before

proceeding.

Before we can let you through to example.com, please complete the following steps:

The post Six million new users in cryptocurrency services in two months appeared first on We Greece.

]]>Nearly 6 million new users have signed up for cryptocurrency services in the first two months of 2021 amid a surge in trading volume and sharp fluctuations in cryptocurrency prices such as Bitcoin and Dogecoin, according to a statement from renowned digital trading platform Robinhood February 25, 2021, cited by a Reuters article.

In 2020, Robinhood cryptocurrency services had an average of about 200,000 new customers trading on its platform each month, according to the company’s blog post

A Robinhood spokesman declined to comment on the total amount of customers trading in the cryptocurrency market through the app, which also offers stock and options trading.

The price of Bitcoin increased by more than 300% in 2020 and this month reached a high of $ 58,354 while the market capitalization jumped from $ 1 trillion.

Dogecoin has also driven a crazy rally driven by the frenzy of micro-investor trading fueled by social media that has pushed up the stock of companies like GameStop.

Dogecoin was created largely to satirize the 2013 cryptocurrency frenzy, it is still traded and its price fluctuates widely.

A tweet earlier this month by billionaire businessman Elon Musk in support of Dogecoin led the currency to rise more than 60%.

Robinhood currently allows customers to buy, sell and hold cryptocurrencies and recently stated that it intends to enable customers to retain and withdraw them in order to transfer them to other “wallets”.

In January, Robinhood angered some of its customers when it temporarily disabled a feature in its app that allowed users to buy instant batteries due to the investment frenzy that accompanied the GameStop case.

Robinhood is expected to make an initial IPO valuation of more than $ 20 billion this year.

The post Six million new users in cryptocurrency services in two months appeared first on We Greece.

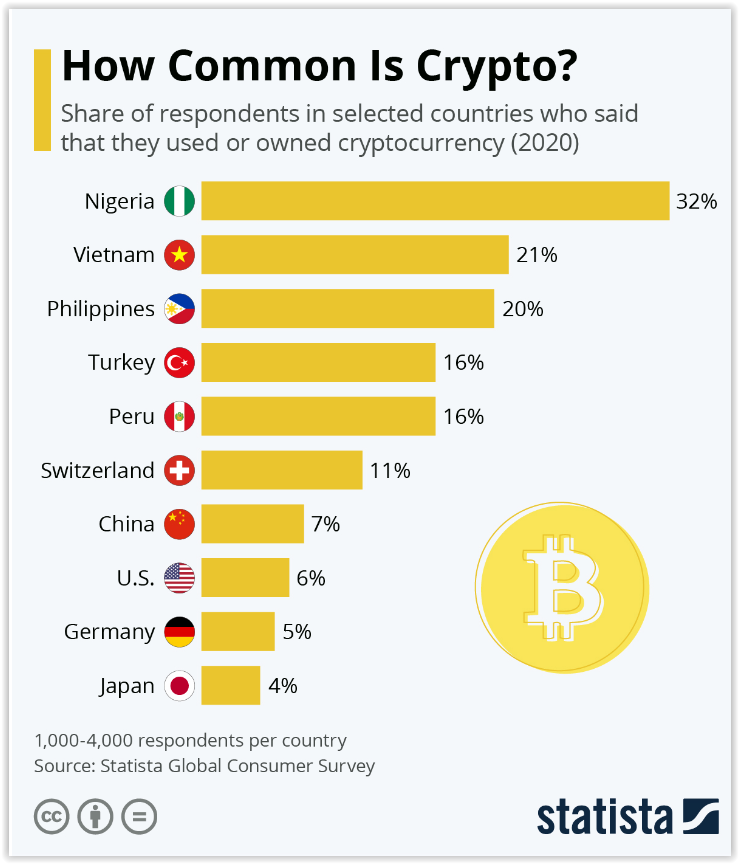

]]>The post Which countries use more cryptocurrencies – At 11% the percentage in Greece appeared first on We Greece.

]]>According to Bitcoin.com it is the high cost of sending money across borders in the conventional way that has led many to turn to cryptocurrency trading.

Nigerians also often use their phones to send money to each other or to pay in stores.

Recently, many companies in the country are adding crypto plugins to their payment options.

The second and third highest percentages of citizens using and / or possessing cryptocurrencies are found in research in Vietnam and the Philippines, respectively.

Again, remittance payments are an important factor for citizens to choose cryptocurrencies.

According to bitcoin.com, the Central Bank of the Philippines has approved the operation of cryptocurrency transfer companies and the government has begun to engage in cryptocurrencies, in cooperation with Unionbank for the distribution of government bonds while Unionbank has also set up a Bitcoin ATM. in Makati, a city in Metropolitan Manila.

Aside from cryptocurrency users in Africa and Southeast Asia, another area that shows a fairly significant preference on them is Latin America.

Peru is the first among these countries with 16% of respondents stating that they use / possess cryptocurrencies while in Brazil, Colombia, Argentina, Mexico and Chile a double-digit percentage is also recorded.

Switzerland and Greece are among the European countries that also record a high percentage, 11%.

Japan again has one of the lowest rates along with Denmark.

The post Which countries use more cryptocurrencies – At 11% the percentage in Greece appeared first on We Greece.

]]>The post American Institute for Economy Research: International Accounting Standards Not Enough for Cryptocurrencies appeared first on We Greece.

]]>One issue that has not yet been addressed is the valuation of cryptocurrencies.

Companies around the world rely on international or national accounting standards, they are the rules of valuation and analysis of assets.

But cryptocurrency accounting as it stands today has no meaning or correlation for businesses.

There are currently no widely accepted valid accounting guidelines for cryptocurrencies.

Some specific countries have implemented unique approaches that stand out, but these are not widely adopted outside of these countries.

In the world of accounting, the two standard-setting bodies are the Financial Accounting Standards Board (FASB) and the International Accounting Standards Board (IASB).

It is true that the IASB has proven to be more flexible in terms of accounting encryption but there are no authentic standards for this purpose.

In the US, and despite significant efforts by the American CPA Institute (AICPA) to publish unauthorized research, the FASB has so far refused to address the issue of cryptocurrency accounting guidance.

Because there are no valid standards, the view has been developed that cryptocurrencies should be treated as an intangible asset of indefinite duration (such as goodwill). At first glance, all this looks good as cryptocurrencies are intangible and do not have a set expiration date.

But analyzing the data quickly reveals how inappropriate this classification is for cryptocurrencies.

According to the accounting rules for intangible assets of indefinite duration, these assets are kept in the balance sheet at the price paid (investment cost) less any impairment charges.

Impairment, without becoming overly technical, is a process by which assets are valued to determine whether or not the carrying amount reflects market value.

If the market value has decreased, the asset is reduced and an expense is recorded in the balance sheet.

According to US accounting standards, there is another side to remember.

Once an asset has been impaired, it cannot be inventoried regardless of what is happening in the market.

This accounting may be good for goodwill, but it does not work for cryptocurrencies.

According to this approach, any organization that invests in cryptocurrencies should record this investment in costs and change it whenever conditions lead to impairment or increase, this is not possible.

Cryptocurrencies are still a volatile market, e.g. in 2021 there were double-digit percentage changes in prices for Bitcoin and countless other cryptocurrencies.

There are two possible solutions that could eventually be applied to companies’ balance sheets given the large fluctuations and valuations of cryptocurrencies.

To treat cryptocurrencies as a commodity-like medium.

It would allow changes in market value to be reported as they appear on the balance sheet and to be reported in the income statement (or as other income).

Applying this approach, modifying existing standards to reflect a new asset class, will increase transparency

A second option, and one that in a perfect world would already be in progress, is to develop entirely new standards for this completely new asset class.

Obviously this would take more time, it would require high levels of cooperation, but the new regulatory framework could make sense.

Classifying different cryptocurrencies according to the case of use (currency alternative, commodity equivalent or equity instrument) would allow new investors to enter.

Accounting professionals need to learn to live and work with encryption and standard accounting standards need to change to incorporate new trends.

Applying standards developed for the 20th century economy to assets that now include cryptocurrencies is unrealistic.

The issue needs to be fixed to avoid future problems

The post American Institute for Economy Research: International Accounting Standards Not Enough for Cryptocurrencies appeared first on We Greece.

]]>

The post Interview of the Vice President of the Hellenic Capital Market Commission for Cryptocurrencies on ERT. appeared first on We Greece.

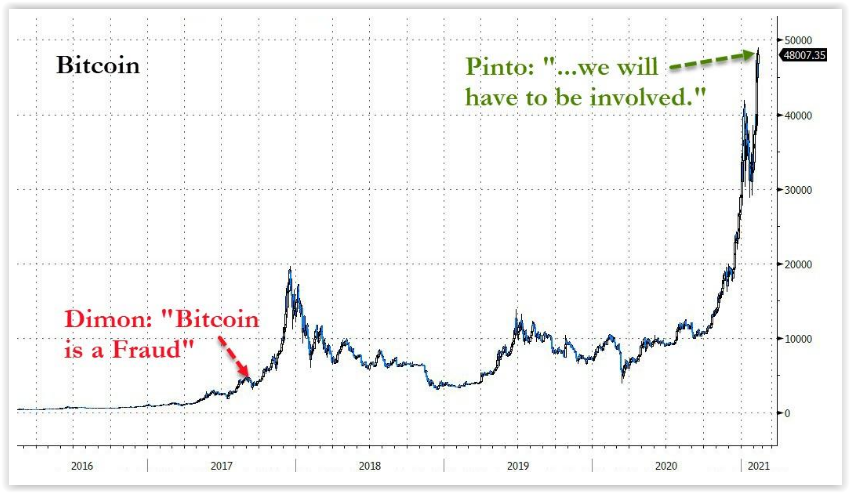

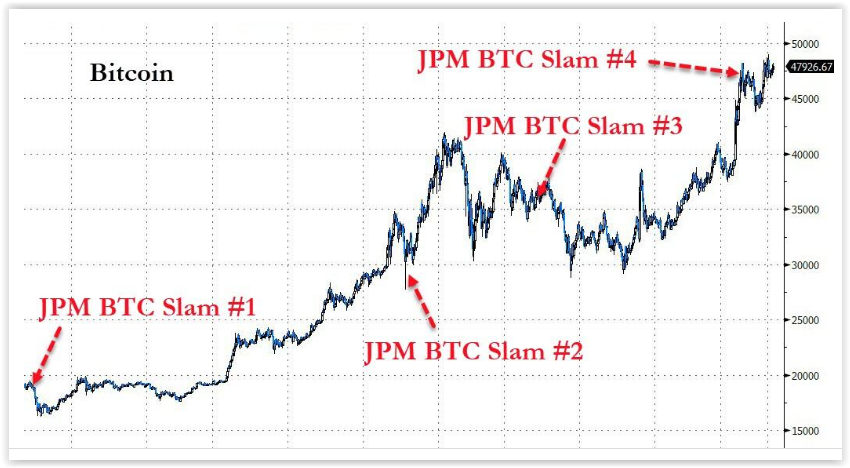

]]>The post JP Morgan’s turn for bitcoin: We have to get involved, we were wrong appeared first on We Greece.

]]>

It is noted that JPMorgan has already failed four times to hit bitcoin.

However, JP Morgan is not the only bank that will be forced to face the new reality of decentralized financing and cryptocurrencies.

According to CNBC, Goldman Sachs organized a private forum with Mike Novogratz, CEO-founder of the cryptographic company Galaxy Digital, for employees and customers.

Novogratz made explanations for bitcoin, ethereum and other currencies.

The post JP Morgan’s turn for bitcoin: We have to get involved, we were wrong appeared first on We Greece.

]]>The post Cryptocurrencies and taxation appeared first on We Greece.

]]>Cryptocurrency is a digital currency without physical form. Today it is produced privately on a computer of modern technology and is distributed through an internet system of advanced technology, the so-called blockchain. In short, everyone can produce their own cryptocurrency, as long as they have the funds, know-how and what is required for the production process. It follows from the above that production is not controlled, is anonymous and independent of Governments and Banks, there are no legal rules and therefore there is no legal protection or guarantee and of course there is a high risk of fraud. In this context, the price of cryptocurrencies fluctuates widely.

As a digital currency, it was established to carry out transactions with simplified procedures in the circulation of money, with greater flexibility, greater speed, lower costs and anonymity in transactions. But in the process it turned out to be an investment product to make a profit from the goodwill (if positive) that is created between the purchase and sale of the currency.

There are two categories of cryptocurrency income:

A) of this producer who does the mining and the income constitutes income from commercial enterprises and the profits that will arise after deducting the operating expenses will be taxed according to the general provisions and the applicable tax rates.

B) Holders of cryptocurrencies

B1) the holder (investor) of cryptocurrencies. Goodwill that may arise (positive difference between purchase and sale) will be taxed under the general provisions if the holders are legal entities.

B2) If the holders are natural persons, ordinary investors believe that according to article 42 of the CFA they will be taxed at a rate of 15% as income from capital gains. Potential loss can be offset by future gains from the same source within the next 5 years.

The taxable value of the cryptocurrency is the goodwill offered by its holder who sells it. Goodwill means the difference between the acquisition price paid by the taxpayer and the sale price received. According to article 42 par. 3, “… any expenses directly related to the purchase or sale of securities are included in the acquisition price and the sale price.”. The tax rate is 15% on the goodwill earned and it is worth mentioning that the income from it is subject to a solidarity contribution.

Taking into account the assumption we made above, that is, that the cryptocurrency is considered an investment-speculative product, the amount allocated for the purchase of cryptocurrencies should be declared in code 743 of table 5 of the tax return (expenditure paid for the purchase of companies, corporations shares and securities in general) of the tax return in order to be included in the calculation of the presumptions. Respectively, the capital from the sale of the cryptocurrencies should be listed in code 781 of table 6 (amounts coming from the disposal of assets and in particular as a return on capital).

In the event that goodwill arose during the sale of the cryptocurrencies, then it should be entered in code 865 of table 4 E (profit from transfer of foreign securities) in order to calculate a 15% tax.

Given the enormous size of the cryptocurrency transaction and its use as an investment derivative, we are confident that there will be a unified international approach to how this investment will be handled by the tax authorities, according to the latest statements of its President. European Central Bank.

Regarding VAT, there is an EU decision which exempts transactions from VAT and on the manner of occurrence of transactions with cryptocurrencies by companies, the 104 / 27.2.2018 opinion of SLOT has been issued for the accounting monitoring of cryptocurrencies to which they approach issue and give directions, but because its implementation is moving in uncharted waters it is logical and expected that many issues will arise for discussion and resolution, and the entire scientific community is waiting for the legislative interventions of the state.

Furthermore, we should point out that the payment of Greek and foreign suppliers in order to recognize the expenses should be paid exclusively through the banking system, therefore the payment in cryptocurrencies is not considered a recognized way of payment for the deduction of expenses.

Finally, due to the structural nature of cryptocurrencies which has been based on encryption, in combination with the anonymity it offers, it has been in several cases to date a transaction of persons associated with illegal-criminal activities and persons who wanted to evade taxes. Identifying the owner by the tax authorities is extremely difficult considering the means required and the know-how needed to detect such activities. Recently, on January 7, with Law 4734/20 on money laundering, the European Directive on the establishment of a register in the Hellenic Capital Market Commission, providers of services for virtual and digital wallets, was incorporated into Greek law.

In closing this article we would like to point out that what we have recorded is our own approach to which we hold every reservation until the issue is finally resolved and of course we should all be cautious until there is a regulatory framework that gives definitive answers to how everything is handled. issues around cryptocurrencies.

* Mr. George Dalianis is the CEO of Artion SA & founder of the Artion Group, Economist – Tax Specialist.

** Mr. Giannis Artsitas is a Senior Accountant – Taxation of Natural Persons of Artion.

The above text is informative and in no way replaces the specialized consulting services.

The post Cryptocurrencies and taxation appeared first on We Greece.

]]>The post The new landscape with the Register for virtual currencies and digital wallets appeared first on We Greece.

]]>Virtual currencies represent a value that is not issued by a central bank or public authority, nor is it guaranteed. It is also not necessarily linked to legally circulating currency and does not have the legal status of currency or money. On the other hand, however, it is accepted by natural or legal persons as a means of transaction and can be transferred, stored or circulated electronically.

Examples of virtual currencies are Bitcoin, LiteCoin, Ethereum, Polkadot etc. used for investment and trading.

The digital wallet is the method (eg a software application) for holding, storing and transferring virtual currencies.

The digital wallet custodian service allows you to participate in the virtual currency system and facilitates transactions in virtual currencies, stores users’ private encrypted keys, holds user account balance in virtual currencies, generally stores virtual currencies and provides transactional security.

Digital wallets can be stored online (hot storage) or offline (cold storage).

It now seeks to regulate the use of virtual currencies and digital wallets by monitoring them by the competent authorities through their providers. The purpose is to control the risk of money laundering within the financial system or within virtual currency networks by terrorist groups and illegal activities.

The Hellenic Capital Market Commission announced at the beginning of the month (January 7) that the providers of virtual and documentary currency exchange services and digital wallet custody must register by January 31, 2021 in the special register, which it keeps [(Law 4557/2018, as amended by Law 4734/2020, to incorporate into Greek legislation Directive (EU) 2018/843 (AMLD V)].

These are:

Register of exchange service providers between fictitious and documentary currencies and

Register of digital wallet custodian service providers.

What is provided for registration

The relevant Registers of the Hellenic Capital Market Commission must be registered, before their activation, the Providers that intend to provide their services in Greece or from Greece to other countries.

The Providers, which are already active in Greece, are subject to the deadline of January 31st.

The entry in the relevant Register includes:

– The application for registration, including information and documents submitted to the EC, for Providers natural and legal persons respectively

– Payment of a fee for the submission of the application and the processing of their registration in the relevant Register

– Annual contribution to cover supervision costs.

Those who do not register by this date will be subject to the sanctions of art. 46 of Law 4557/2018, as a fine, a public announcement stating the person and the nature of the violation, but also prohibitions that may reach the final prohibition of the provision of these services.

The post The new landscape with the Register for virtual currencies and digital wallets appeared first on We Greece.

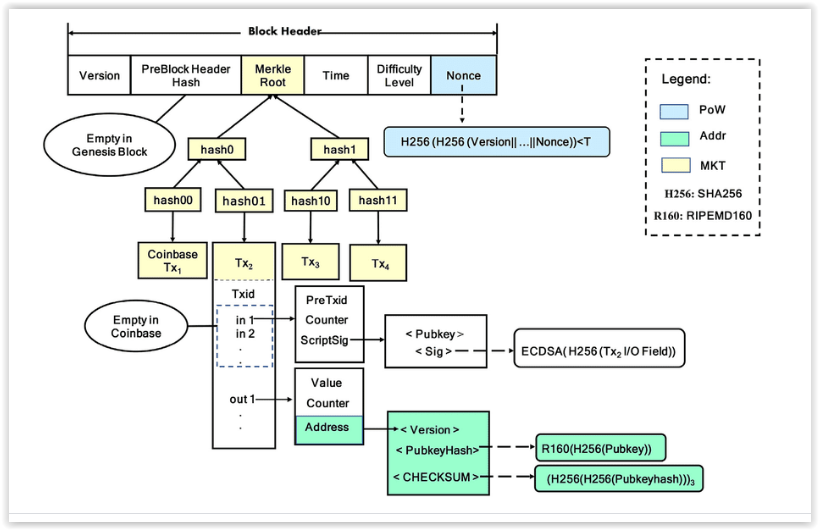

]]>The post Why Nobody Can Hack a Blockchain appeared first on We Greece.

]]>A common mistake that new cryptocurrency investors make is to confuse the hacking of a blockchain with that of a digital exchange. Whereas unfortunately centralized digital exchanges get hacked more than they should, decentralized blockchain hacks are very rare, as they are hard to achieve and provide little incentive to carry out.

In this post, we look at what makes blockchains — as applied in the cryptocurrency sector — impervious to security breaches.

The blockchains behind most cryptocurrencies are peer-to-peer (P2P), open-source and public, allowing everyone with the right equipment and knowledge to peek in under the hood. This is important to foster transparency and attract buyers.

A blockchain comprises different technological mechanisms working together towards a common goal. For instance, there are consensus mechanisms such as proof of work (PoW) and proof of stake (PoS) that protect the network by mitigating cyber-attacks from hackers.

A blockchain’s decentralized nature means that its network is distributed across multiple computers known as nodes. This eliminates a single point of failure. In other words, there is no way to “cut the head off the snake” — because there isn’t any head.

The architecture of a blockchain determines how the nodes cooperate in verifying a transaction before being committed to the protocol. In the case of Bitcoin and other PoW systems like Bitcoin Cash, a minimum of 51% of the nodes must agree to the transaction before commitment.

Each transaction is called a block, and the interconnection of several transactions becomes a blockchain. Notably, a block has cryptographic elements that make it unique. A network’s hashing algorithm determines the details. For example, the Bitcoin blockchain uses the double SHA-256 hash function, which takes transaction data and hashes/compresses it into a 256-bit hash.

By making it hard to reverse the hashed value, a transaction becomes inflexible. Each block in a chain contains a specific set of data from the previous block. Therefore, even if a malicious actor reverse-engineers the hash, the resultant block would be out of sync with the rest of the blocks since it will have a different hash output, thus causing the system to reject it.

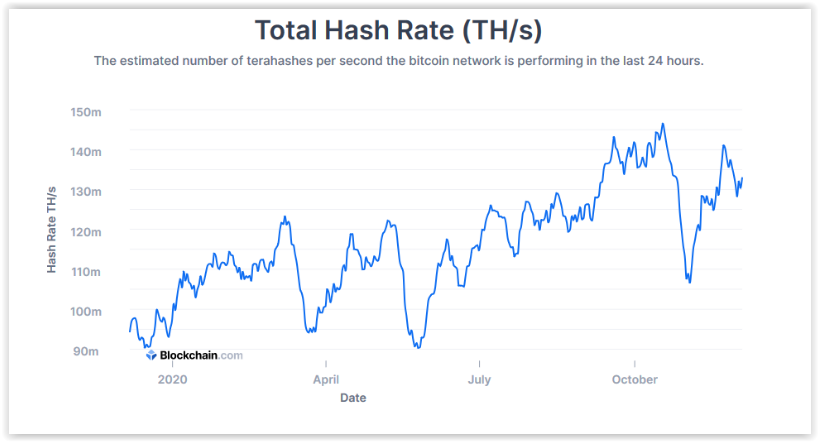

The longer a blockchain exists and the more new users it attracts, the less likely it is to suffer a 51% attack due to its growing hash power.

This becomes prohibitively expensive at a certain point. Therefore, considering the size of established blockchains like Ethereum and Bitcoin, such a scenario is nearly impossible.

Another reason why it’s even harder to hack a blockchain is that in case the block being re-hashed is at the middle of the chain, the attacker would have to re-hash previous blocks to align their historical stamp with the new block.

For Bitcoin, this is only possible with the next generation of quantum computing, which currently doesn’t exist. And even when it does, who’s to say there won’t be a blockchain-based quantum defense mechanism to mitigate quantum attacks?

In PoS-based systems, stakes determine the strength of the network. To elaborate, this means those users who have delegated or actively locked their native blockchain assets to participate in transaction processing and finding new blocks. On such systems, an attack occurs when a hacker controls a majority of the stake.

This is possible when the hacker accumulates over 51% of all coins in circulation. For reputable networks like the evolving Ethereum 2.0 platform, this is all but impossible. Imagine trying to find the funds to buy up 51% of ETH’s current $68 billion market cap!

You can’t orchestrate a stealth 51% attack without creating too much scarcity, as your purchasing of coins will make the available ones skyrocket in value to incredibly high levels. Conversely, when the blockchain participants find out you own a majority of the coins, they will likely sell their holdings, thereby crashing the market with excess supply. So you’ll end up buying high, and selling low!

Good question. It boils down to the strength of a network. Notable 51% attack victims include Ethereum Classic, Bitcoin Gold, Electroneum, and most recently Grin. The Ethereum Classic network uses the PoW consensus algorithm. Although Bitcoin uses the same algorithm, ETC has a much lower number of nodes and miners securing the system. Thus, it has lesser processing power, making it easier for an attacker to take control.

ETC has a hash rate of 1.6 tera hash per second, while Bitcoin’s stands at 117.9 exa hashes per second.

So far, nobody has single-handedly hacked a blockchain. Instead, it’s usually a group of malicious actors or the core dev team that collaborate to breach a blockchain’s security. However, as blockchain platforms get stronger through an increase of nodes or stakers, the possibility of hacking a decentralized network is increasingly moving towards zero.

In addition, newer blockchain systems use academically-proven techniques that would need highly-specialized quantum computers to hack.

To sum it all up — if you ever hear someone saying that a “blockchain was hacked!” you now have the tools to (politely) correct them and send them on their way.

The post Why Nobody Can Hack a Blockchain appeared first on We Greece.

]]>The post Bitcoin hits new record high appeared first on We Greece.

]]>The post Bitcoin hits new record high appeared first on We Greece.

]]>The post One of the world’s top banks issues bonds that can be bought with Bitcoin appeared first on We Greece.

]]>One of the “Big Four” banks in the People’s Republic of China, CCB is ranked the second-largest bank worldwide by total assets as of fall 2020.

The megabank’s plan with the new blockchain-based debt issuance is to raise up to $3 billion in total, starting with a tranche of $58 million, from individuals and institutions. The digital bonds will be issued through an offshore branch of CCB in Labuan, Malaysia, at a minimum of as little as $100 each, and will have a tenor of three months. They pay an annualized interest of Libor plus 50 basis points, or roughly 0.75%.

The innovation is that these bonds are being used as tokenized certificates of deposit on the blockchain, which supports the issuance of such small-sum bonds; non-blockchain-based bonds are typically sold at higher minimums, and are therefore limited to professional investors or other banks.

Moreover, the tokenized certificates of deposit will be tradable on the Fusang exchange. The exchange, which is regulated in Labuan, will launch live trading of the bonds on Nov. 13. Notably, as Fusang supports cryptocurrency trading, traders will be able to exchange Bitcoin (BTC) for U.S. dollars in order to purchase the bonds. The transactions will be charged at a commission.

Fusang’s CEO Henry Chong has told reporters that if the bonds are popular, the digital exchange intends to initiate similar products denominated in other currencies. The bonds’ 0.75% annualized interest is higher than most U.S. dollar bank-deposit rates, as the Wall Street Journal has emphasized.

Tax residents of the United States and China, as well as entities or persons in Iran and North Korea, will not be able to purchase the digital security. All proceeds from the issuance will be deposited at the CCB’s offshore Labuan branch. Labuan is a small island described by the Wall Street Journal as a tax haven.

CCB is “not dealing in bitcoin or cryptocurrencies,” but rather “taking bank deposits, which is our core business,” CCB Malaysia’s chief operating officer Steven Wong stressed. The offering is nonetheless being heralded as a big innovation. This is “the first publicly listed debt security on a blockchain,” said Felix Feng Qi, the CEO of CCB’s offshore Malaysian business and principal officer of the CCB Labuan branch.

The post One of the world’s top banks issues bonds that can be bought with Bitcoin appeared first on We Greece.

]]>